Understanding Income Tax in NZ: A Clear Guide for 2026

- Peter Eastmure

- Feb 22

- 11 min read

Updated: Mar 24

For many individuals and business owners, managing income tax in NZ can be a source of significant uncertainty. The official information often feels dense and difficult to interpret, leading to valid concerns about compliance, potential penalties, and whether you are paying the correct amount. Accounting should not be a source of stress; it should provide clarity and control.

This guide, brought to you by Eastmure & Associates Limited, is designed to deliver that clarity. We provide a comprehensive and direct overview of the New Zealand income tax system for the 2026 financial year, tailored for individuals and business owners. We will demystify the core components of the system, from understanding the correct tax rates that apply to you to navigating your obligations around provisional tax and meeting crucial deadlines.

Our goal is to equip you with the knowledge to manage your tax affairs proactively and with confidence. You will gain a precise understanding of how tax is calculated, how to ensure full compliance, and how to identify strategic opportunities to legally minimise your tax exposure, providing you with greater peace of mind.

Key Takeaways

Understand how New Zealand's progressive tax brackets for the 2024-2025 year apply to your specific level of income.

Clarify your core tax obligations, which differ significantly depending on whether you are a salaried employee, a contractor, or a business owner.

Identify the critical deadlines for filing your income tax nz return to ensure timely compliance and avoid unnecessary penalties.

Move beyond simple compliance by learning how proactive tax planning can become a strategic financial management tool.

Table of Contents What is Income Tax? The Fundamentals for New Zealanders NZ Income Tax Rates and Brackets for the 2024-2025 Tax Year How Tax is Managed for Different Types of Earners Key Income Tax Deadlines and Payment Obligations Beyond Compliance: Strategic Approaches to Income Tax

What is Income Tax? The Fundamentals for New Zealanders

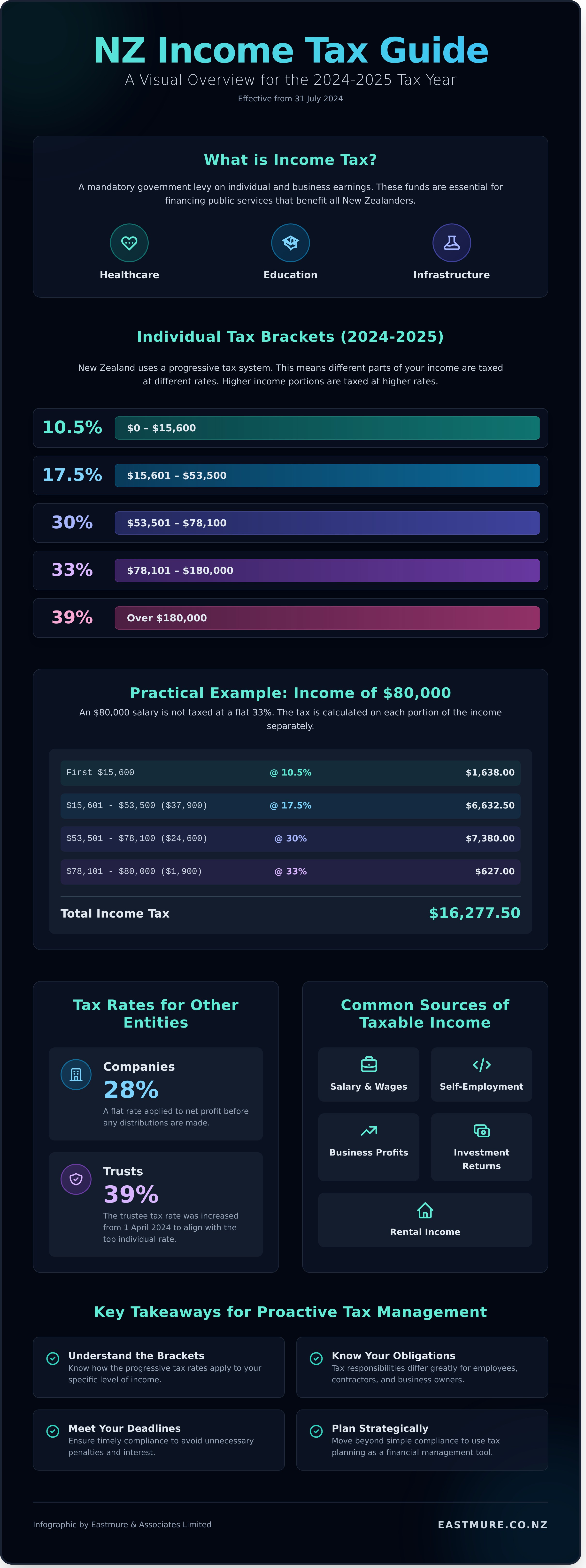

Income tax is a mandatory contribution levied by the government on the earnings of individuals and businesses. Navigating the requirements for income tax nz can seem complex, but its core principles are designed to be methodical. The funds collected are essential for financing public services that benefit all New Zealanders, including healthcare, education, and infrastructure.

New Zealand operates a progressive tax system. Think of your income filling a series of buckets; the first portion of your earnings is taxed at the lowest rate. Once that bucket is full, any additional income flows into the next bucket, which is taxed at a higher rate, and so on. This structure ensures that higher earners contribute a larger percentage of their income in tax. This is a central component of the wider system of Taxation in New Zealand, and it is important to distinguish it from other levies like Goods and Services Tax (GST) or ACC contributions.

Taxable Income Explained

The Inland Revenue Department (IRD) defines 'taxable income' as any income on which you are required to pay tax. While this often refers to salary or wages, it encompasses a broader range of sources, including:

Income from self-employment or contracting

Business profits

Investment returns, such as interest and dividends

Rental income from property

For businesses, it is critical to understand that tax is calculated on profit (revenue minus allowable expenses), not total revenue. Identifying these allowable deductions is a key step in ensuring accurate compliance.

Understanding Your Role and Responsibilities

As a taxpayer, your primary responsibility is to provide complete and accurate information to the IRD in a timely manner. The IRD's role is to administer the tax system, collect revenue, and ensure all parties meet their obligations. A tax agent, such as a chartered accountant, acts as a professional intermediary. Their function is to provide strategic advice, ensure meticulous compliance with all regulations, and represent your interests, delivering clarity and peace of mind in your financial affairs.

NZ Income Tax Rates and Brackets for the 2024-2025 Tax Year

Understanding New Zealand's marginal tax rate system is fundamental to effective financial planning and ensuring full compliance. Your total income is not taxed at a single rate; instead, different portions of your income are taxed at progressively higher rates as you move through the brackets. This structure is designed to be equitable, but it requires careful management to optimise your tax position. For a complete official reference, the Inland Revenue Department details all NZ income tax rates and obligations on its website.

Individual Tax Rates (2024-2025)

The following table outlines the individual tax rates for the tax year 1 April 2024 to 31 March 2025. Please note that these thresholds are effective from 31 July 2024, reflecting the most recent government adjustments.

Annual Income Bracket (NZD) Tax Rate $0 - $15,600 10.5% $15,601 - $53,500 17.5% $53,501 - $78,100 30% $78,101 - $180,000 33% Over $180,000 39%

Practical Example: An individual earning an annual salary of $80,000 does not pay a flat 33% on their entire income. Instead, their tax is calculated progressively:

The first $15,600 is taxed at 10.5%.

The portion from $15,601 to $53,500 is taxed at 17.5%.

The portion from $53,501 to $78,100 is taxed at 30%.

Only the income from $78,101 to $80,000 is taxed at the 33% rate.

This marginal system ensures you only pay the higher rate on the income that falls within that specific bracket, providing clarity on your overall income tax NZ liability.

Tax Rates for Other Entities

Beyond individual income, different legal structures are subject to distinct tax rates. This distinction is critical for strategic business and asset planning.

Company Tax Rate: Companies in New Zealand are taxed at a flat rate of 28% on their net profit before distributions.

Trust Tax Rate: The trustee tax rate has been set at 39% from 1 April 2024. This aligns the top trust rate with the top individual marginal rate, a significant change impacting wealth protection and asset structuring strategies.

These flat rates differ from the progressive individual system because companies and trusts are separate legal entities. The choice of structure-whether operating as a sole trader, company, or trust-has profound implications for minimising tax exposure and protecting your assets over the long term.

How Tax is Managed for Different Types of Earners

Understanding your tax position begins with recognising how you earn your income. The structure of your earnings dictates the level of responsibility you hold for managing your tax affairs. For many, the process is automated; for others, it requires meticulous, proactive management. How you manage your income tax nz obligations shifts significantly as you move from employment to self-employment and business ownership.

For Employees: The PAYE System

For most salaried and waged employees in New Zealand, tax is managed through the Pay As You Earn (PAYE) system. Your employer deducts income tax directly from your pay and forwards it to Inland Revenue (IR) on your behalf. The amount deducted is determined by the tax code you provide, which reflects your personal circumstances. For the majority of employees with a single source of income, this process seamlessly meets their annual tax obligations without any further action required. However, you may need to file a return if you:

Receive income from other sources, such as rentals or investments.

Have earned income from more than one employer.

Used an incorrect tax code during the year.

For Sole Traders & Contractors: Taking Control of Your Tax

As a sole trader or independent contractor, the responsibility for compliance shifts entirely to you. You are required to calculate and pay your own income tax nz, typically through provisional tax instalments throughout the year. This proactive approach prevents a large tax bill at the end of the financial year. Success in this structure depends on meticulous record-keeping of all income and claimable business expenses. It is also your responsibility to manage and pay separate ACC levies based on your earnings.

For Companies and Trusts: Separate Legal & Tax Entities

A registered company is a separate legal entity from its owners and is taxed on its own profits at the current company tax rate of 28%. Profits can then be distributed to shareholders as dividends, which are subject to further tax rules. Trusts introduce another layer of complexity, with tax obligations depending on how income is generated and distributed to beneficiaries. Navigating these structures requires precision and strategic foresight to ensure compliance and tax efficiency. Structuring your affairs correctly is critical. We provide discreet advice.

Key Income Tax Deadlines and Payment Obligations

Meeting your tax obligations with precision is fundamental to sound financial management. In New Zealand, the tax system operates on a clear annual cycle, but understanding the distinction between filing a return and paying the tax owed is critical for maintaining compliance and avoiding unnecessary penalties. A proactive approach ensures that your income tax nz obligations are met seamlessly, providing clarity and peace of mind rather than stress and uncertainty.

The Financial Year and Filing Dates

New Zealand's standard financial year runs from 1 April to 31 March. For individuals who file their own tax return, the deadline is typically 7 July following the end of the financial year. However, engaging a tax agent provides a significant and strategic advantage: an Extension of Time (EOT). This automatically extends your filing deadline to 31 March of the next year, providing ample time for meticulous preparation and review. While most entities use this standard date, some businesses may secure approval from Inland Revenue for a different financial year.

Understanding Tax Payments: Provisional vs. Terminal

Navigating payment deadlines requires clarity on two key concepts. It is crucial to remember that a filing deadline is for submitting your information, whereas a payment deadline is for settling your liability with Inland Revenue.

Terminal Tax: This is the final tax payment, or "wash-up," for the previous financial year. It reconciles the provisional tax you have already paid with your actual final tax liability. The standard due date is 7 February.

Provisional Tax: These are pre-payments made towards your current year's expected income tax liability, designed to manage tax flow throughout the year. For most, these payments are due in three instalments on 28 August, 15 January, and 7 May.

Failing to meet these deadlines has consequences. Late filing can incur penalties starting from NZ$50, while late payment attracts compounding interest and further penalties. Working with a specialist ensures these distinct obligations are managed deliberately. The primary benefit of using a tax agent is the extended filing deadline, but for many of our clients, the terminal tax due date is also extended to 7 April, offering valuable cash flow flexibility and reinforcing financial stability. For strategic advice on your tax compliance, contact our specialists.

Beyond Compliance: Strategic Approaches to Income Tax

Meeting your tax obligations is the baseline of financial management, but the true opportunity lies in shifting from a reactive to a proactive approach. For discerning individuals and business owners, tax is not merely a compliance task; it is an area for strategic planning designed to enhance wealth protection and achieve long-term financial stability. A forward-thinking strategy transforms your relationship with income tax in NZ from an obligation into an opportunity for efficiency.

The Power of Legitimate Deductions

The fundamental principle of tax deductions is that you can claim expenses incurred in the course of generating your assessable income. Meticulous record-keeping is paramount. For businesses, this often includes a portion of vehicle running costs, home office expenses, professional subscriptions, and capital allowances on assets. However, it is critical to maintain a clear distinction between business and private expenditure. Attempting to claim personal expenses is a significant compliance risk, and robust proof-such as invoices and receipts-is non-negotiable for every claim.

Structuring for Tax Efficiency

Your choice of business structure-be it sole trader, partnership, company, or trust-has profound and lasting implications for both your tax liability and your personal asset protection. The optimal structure is not static; it should be reviewed as your income grows, your family circumstances change, or your business evolves. While a company may offer a lower tax rate, a trust can provide superior asset protection. This is a complex decision where professional guidance is essential to align your structure with your strategic goals.

When to Engage a Professional Tax Advisor

While straightforward tax affairs can often be self-managed, certain events and complexities are clear triggers for seeking specialist advice. Engaging an advisor is a prudent investment when you are:

Starting, purchasing, or selling a business.

Entering a high-income bracket with more complex tax obligations.

Investing in residential or commercial property.

Managing income from trusts, estates, or overseas sources.

Planning for succession or retirement.

The cost of professional advice should be viewed as an investment in confidence, compliance, and financial efficiency. Our expertise is in providing clarity for complex financial situations. We deliver the foresight and precision required to ensure your financial affairs are managed deliberately and effectively.

From Understanding to Strategy: Mastering Your NZ Tax Obligations

Grasping the fundamentals of New Zealand's tax system is the essential first step. As we've explored, understanding the 2024-2025 tax brackets and your specific compliance deadlines provides a solid foundation. However, true financial control moves beyond simply meeting obligations and into the realm of proactive, strategic planning.

For medical professionals and high-net-worth individuals, managing the complexities of income tax nz demands more than a reactive approach. It requires foresight and precision to not only ensure compliance but to strategically protect and grow your wealth for the long term. This shift from obligation to opportunity is where genuine peace of mind is found.

Our specialist tax advisors deliver this with absolute discretion and meticulous attention to detail. For clarity and confidence in your tax obligations, schedule a confidential consultation. Let us help you build a secure and prosperous financial future.

Frequently Asked Questions

Do I have to file an income tax return in NZ if I'm a salaried employee?

In most cases, if your only source of income is from salary or wages where tax (PAYE) is deducted, Inland Revenue will issue an automatic assessment, and you do not need to file a return. However, a return is mandatory if you have other income, such as from a rental property, self-employment, or overseas. Filing may also be advantageous if you wish to claim expenses or believe you have overpaid tax during the year.

What is the difference between income tax and GST?

Income tax is a direct tax levied on the net income of individuals and businesses. It is calculated on profits and earnings over a financial year. In contrast, Goods and Services Tax (GST) is an indirect tax of 15% applied to the price of most goods and services. Businesses registered for GST collect this tax on behalf of the government from consumers and remit it to Inland Revenue, typically on a two-monthly or six-monthly basis.

What happens if I can't pay my tax bill on time?

If you anticipate difficulty in paying your tax on time, it is crucial to communicate with Inland Revenue proactively. Ignoring the obligation will result in penalties and interest charges. By contacting them early, you may be able to establish a formal instalment arrangement to manage the debt. A strategic approach provides clarity and control, helping you maintain compliance while navigating financial pressures and securing your peace of mind.

Can I claim work-from-home expenses against my income tax?

For salaried employees, work-from-home expenses are generally not claimable. However, if you are self-employed, a contractor, or a business owner operating from home, you can claim a portion of relevant household costs. This can include utilities, insurance, and mortgage interest, calculated precisely based on the area of your home dedicated to business use. Meticulous record-keeping is essential to substantiate these claims for your income tax nz return.

How do I find out my IRD number?

Your Inland Revenue Department (IRD) number is a critical identifier for all tax-related matters. It can be found on correspondence from Inland Revenue, such as a statement of account or a summary of income. It is also often included on payslips provided by your employer. If you cannot locate it through these documents, you can retrieve it by logging into your secure myIR online account or by contacting Inland Revenue directly with sufficient proof of identity.

What is the fastest way to get my tax refund?

The most efficient way to receive a tax refund is to ensure your details with Inland Revenue, particularly your bank account number, are correct and current. Using the myIR online portal for any filings significantly accelerates the process. For individuals with complex financial structures, engaging a tax professional ensures the return is prepared with precision and lodged correctly, providing confidence and facilitating a prompt and accurate refund from Inland Revenue.

Comments